The latest headline from the newsreel has been regarding inflation and how rising prices could place a strain on the US economy. Indeed, the Producer Price Index, which measures the prices of a variety of input products for US manufacturing (including metals, agricultural products, and fuel products) has been steadily increasing for the last two years. Similarly, we all have noticed that the price to fill up our car’s gas tank is higher than it was over the same time period. In fact, the price of gasoline, if you purchase it directly from the commodities market, has climbed to $2.12/gallon – the most expensive since late 2014. You might stop and say “hold on, I paid $3.00/gallon at the pump last week!” Well, you have to factor in the cost of transporting it to and storing it at your local gas station as well as the roughly $0.77/gallon in taxes imposed on your purchase.

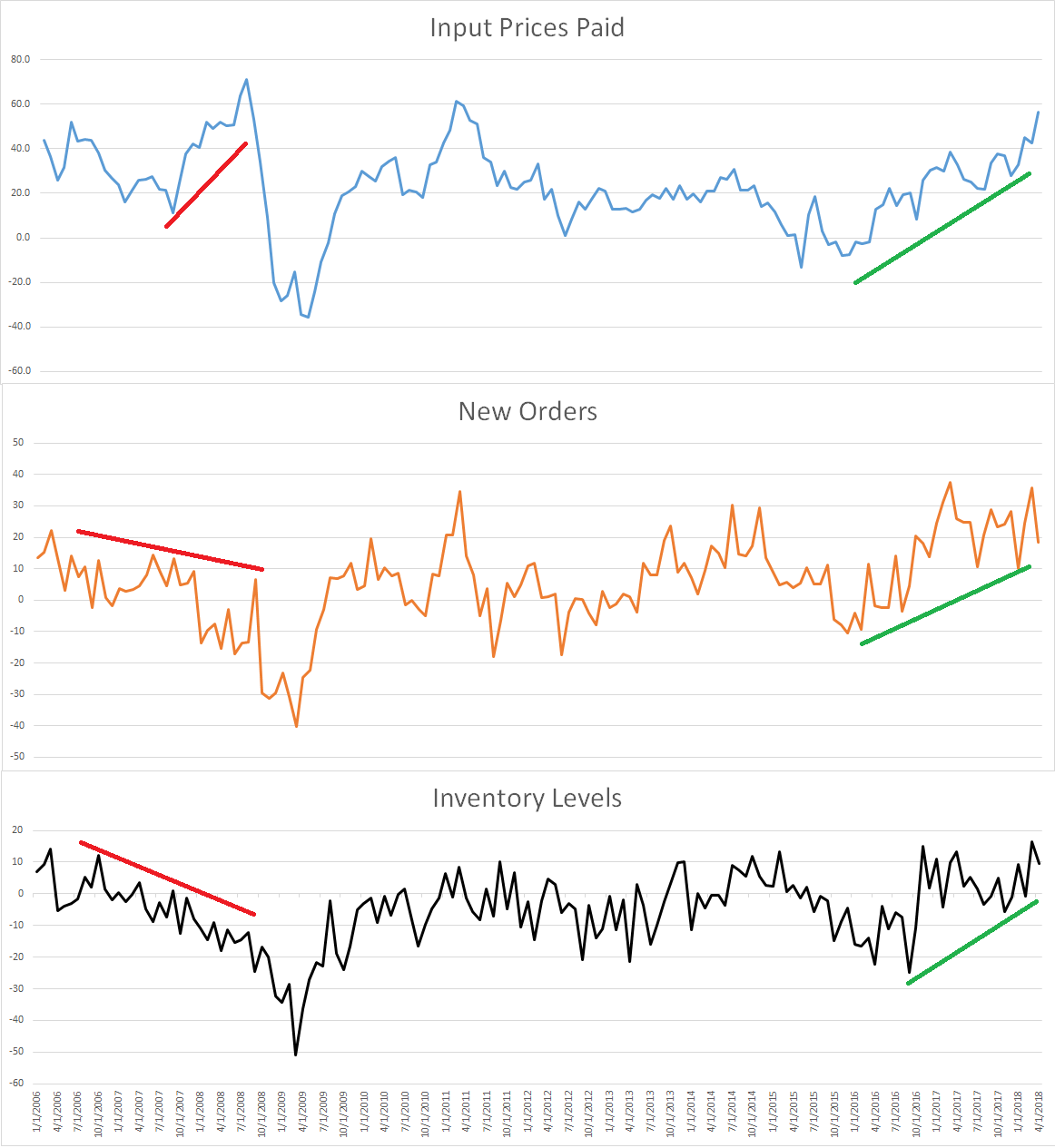

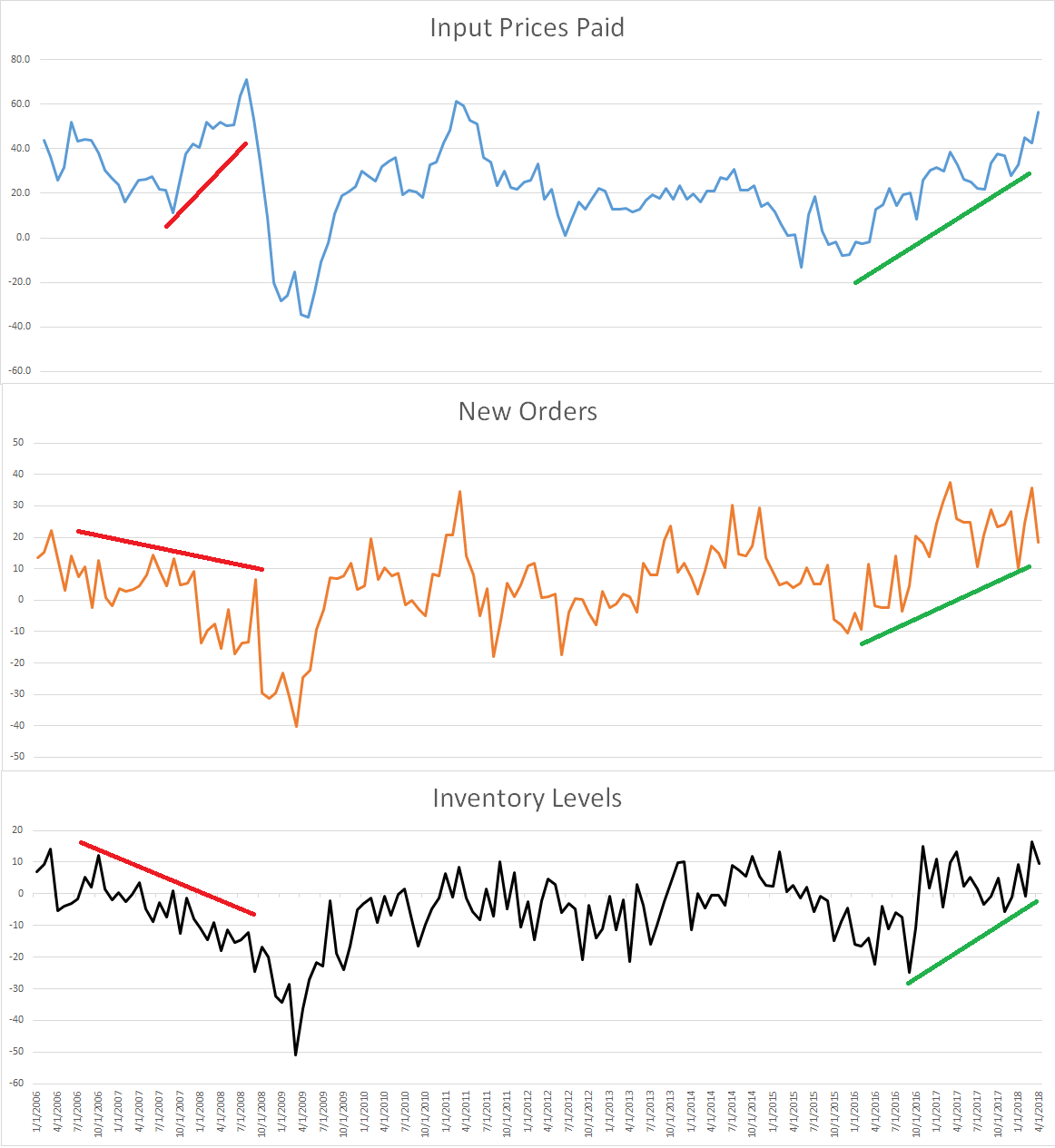

We digress. The concern facing investors is that rising prices can hurt an economy’s prospects for growth. Stagflation in the 1970s and the oil price bubble in 2008 could be pointed out as two extreme examples. These investors, however, are only looking at part of the equation. Rising prices alone are not bad; they are even often associated with an improving economy and increasing wages for workers. Increasing prices (i.e. inflation) only becomes a problem when consumers and businesses can’t afford to purchase the goods and services they need to thrive. Below is an example, which uses data from a business survey conducted by the Philadelphia Federal Reserve. They ask business executives, among other questions, if they are receiving more/fewer new orders, if they are increasing their inventories in anticipation of future sales, and if the costs to create goods are increasing or decreasing. Below are their indexes for these items. Data has been included back to 2006 to contrast today’s environment to the economy just prior to the Great Recession.

The left side of the charts reflects the business environment before the Great Recession. As early as 2006, the number of new orders placed was decreasing and inventories were shrinking too. These created less-than-ideal economic conditions, and when input prices spiked higher in 2007 and 2008, it was to enough to make businesses unprofitable and drag the economy into a recession.

Contrast that to today’s environment, which can be observed on the right hand side of the chart, and a healthier economy can be observed. Prices are rising, but new orders and inventories are also gradually increasing. This means that even though it’s more expensive to produce goods and services, businesses are still flush with orders to fill from eager customers, even if these businesses decide to charge customers more to offset higher production costs. In 2008, the situation was the opposite. Not only were customers disinterested in creating new orders, but businesses also found themselves having to pay high prices for the relatively few orders needing to be filled.

In summary, yes, signs of inflation are apparent, and inflation can have the ability to damage an economy and hurt investors’ portfolios. However, in this case, the threat of rising prices is currently being offset by a strong base of new orders. As long as these trends remain intact, and we will be closely monitoring this data, the threat of rising prices to the health of the economy and stock market should be subdued.